Official Market Statement from LYTH

As a lithium battery exporter serving Europe, the United States, Australia and Southeast Asia, LYTH supplies LFP, NMC, SIB and LTO cells and modules for ESS, mobility and industrial applications.

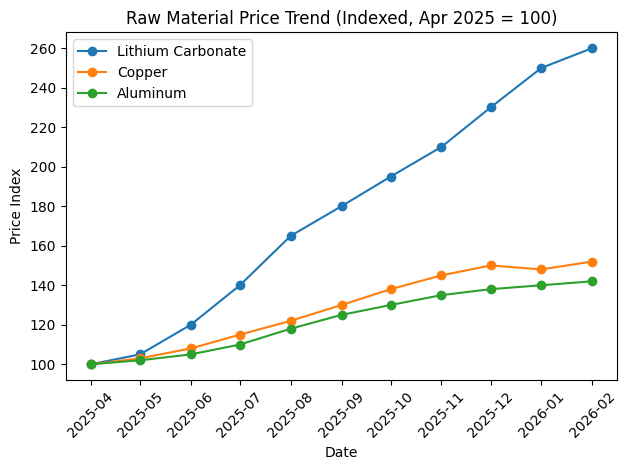

Over the past eight months, lithium carbonate prices have rebounded sharply from historical lows. Meanwhile, copper, aluminum and graphite costs have increased, fundamentally reshaping the cost structure of battery cells.

Structural Cost Shift

Industry cost models for 314Ah cells indicate:

Cathode material share has increased significantly

Copper foil and structural component costs have risen

Low-cost inventory has largely been digested

This is no longer a short-term fluctuation. It is a structural reset of cost baselines.

Export Policy & Demand Front-Loading

The export tax rebate transition period before April 2026 has accelerated overseas procurement cycles. Available production capacity is tightening, and quotation validity periods are shortening accordingly.

For project-driven markets such as the EU, US and Australia, delayed purchasing decisions may translate into direct budget adjustments.

2026 Price Outlook

Industry signals suggest:

The price floor has shifted upward

Unsustainable below-cost pricing is ending

Supply will increasingly favor companies with scale and vertical integration

A return to previous price lows appears unlikely under current demand dynamics.

Our Commitment

At LYTH, we remain:

Transparent in cost logic

Responsible in delivery commitments

Focused on long-term partnerships

Supportive of internal technical and financial evaluations

We encourage partners with confirmed or upcoming projects to consider early capacity allocation and pricing confirmation, reducing exposure to further volatility.

In the current cycle, execution stability outweighs temporary price advantages.

LYTH Ships 40,000 CALB LFP Cells via Horgos, Expanding Global Energy Supply Routes

LYTH Ships 40,000 CALB LFP Cells via Horgos, Expanding Global Energy Supply Routes LYTH Completes Delivery of 100 Bespoke 1P12S NMC Battery Modules

LYTH Completes Delivery of 100 Bespoke 1P12S NMC Battery Modules Why Precision Matters? Behind LYTH’s Latest 5,000-Cell Shipment to Austria

Why Precision Matters? Behind LYTH’s Latest 5,000-Cell Shipment to Austria 2026 Cell Price Update | Structural Cost Repricing Underway

2026 Cell Price Update | Structural Cost Repricing Underway