» Our Blog » US Lithium Battery Import Tariff Increase

US Lithium Battery Import Tariff Increase

April 10, 2025

US lithium battery import tariff increase:

A new energy game that affects the world

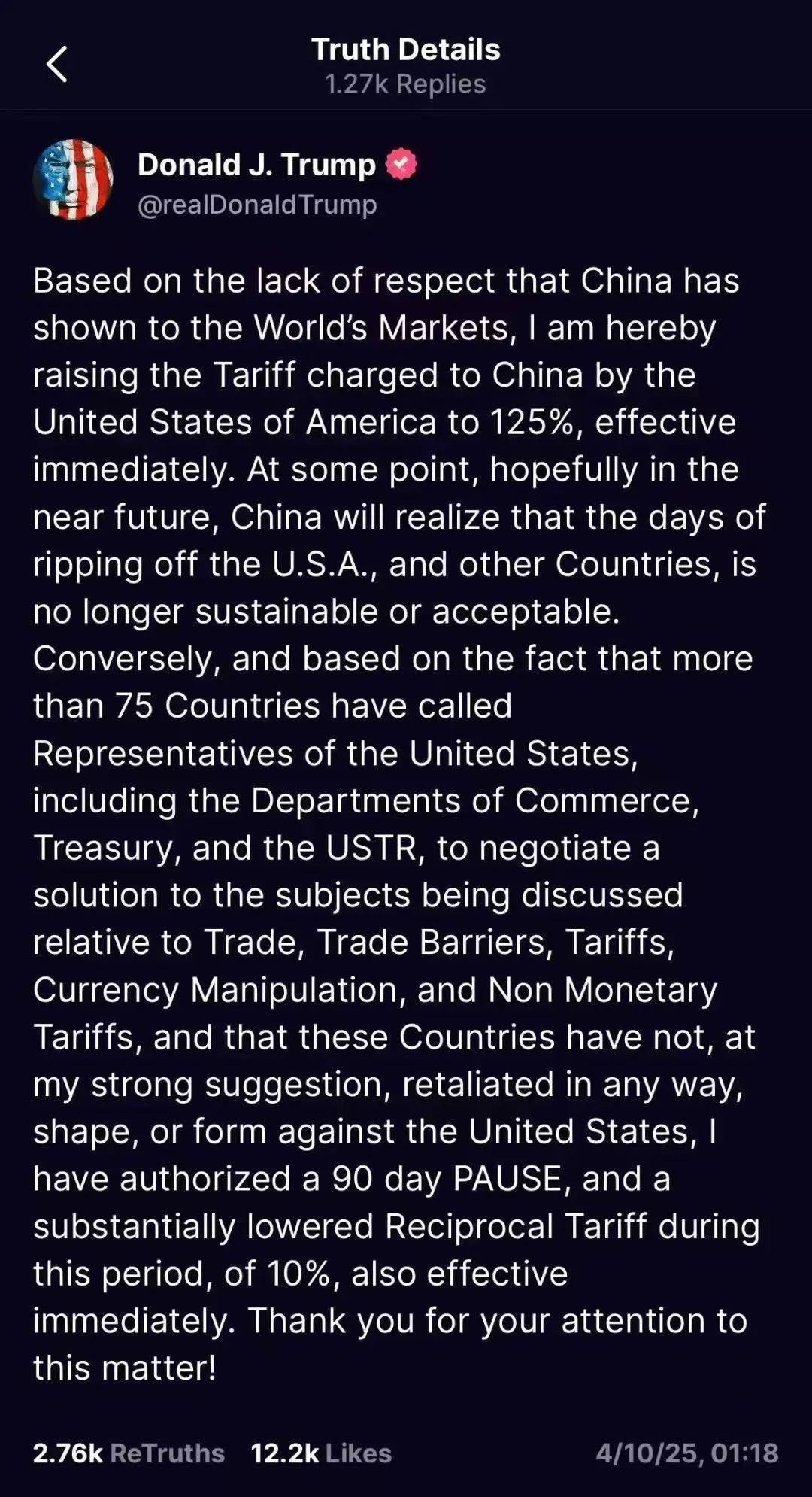

On 10 April 2025, United States President Donald Trump announced via social media his decision to raise tariffs on imports originating in China to 125%, effective immediately. Earlier, the US government had announced an increase in ‘reciprocal tariffs’ on Chinese exports to the United States from 34% to 84% , effective 9 April. The Government of China responded swiftly by announcing that, effective 10 April 2025, the tariff rate on imports of United States origin would be increased from 34% to 84%.

* The ‘secret struggle’ behind tariffs: what is the United States fighting for?*

The original intention of the United States to raise tariffs on lithium batteries, pointing directly to the two core objectives: ‘industrial reflux’ and ‘energy security’.

Local manufacturing ambitions: Over the past decade, the United States has accounted for only 6% of the world’s lithium battery production capacity, relying heavily on imports (China accounts for 75% of global capacity). The tariff hike is intended to force Car companies and battery manufacturers to relocate their production lines to the US, replicating the path of the Chip Act in the semiconductor industry and reviving manufacturing.

A microcosm of geopolitical rivalry: Behind the policy are concerning about China’s dominance of the new energy chain. The US is trying to weaken import dependence through tariff barriers, while pushing its allies (e.g., South Korea’s LG, Japan’s Panasonic) to accelerate the construction of factories in the US and build a ‘de-Chinaised’ supply chain.

Controversial point: the policy seems to protect local enterprises, but the United States in the short term lack of complete lithium materials refining and battery production capacity, forced ‘decoupling’ may lead to supply shortages. Tesla CEO Musk has publicly questioned, ‘Raising tariffs is like putting the brakes on the electric car industry.’

* The ‘butterfly effect’ of the industrial chain: who benefits? Who gets hurt?*

1. Local U.S. companies: both opportunities and risks

Short-term pain: EV companies relying on imported batteries (e.g., Rivian, Lucid) are facing soaring costs, and may be forced to increase prices of some models by 5-10 per cent, undermining market competitiveness.

Long-term dividends: stimulated by the policy, Chinese companies such as CATL and Svolt are accelerating their co-operation with Ford and Tesla to build factories through the technology licensing model; South Korea’s SK On and Samsung SDI have announced additional investment in the US, and the local production capacity is expected to triple by 2030.

2. Consumers: paying for ‘energy independence’?

Electric vehicle price hikes could slow down the pace of penetration and run counter to the target of 50% electric vehicle penetration by 2030. But if the local supply chain matures and costs come down, there is still room for imagination in the long term.

Emotional resonance: One US user tweeted on social media, ‘The government always says “Buy American”, but my wallet only cares about when I can buy a $30,000 affordable electric car.’

3. Global Supply Chain: Reconstruction and Breakout

Chinese battery enterprises have turned to Mexico and Southeast Asia to build factories and avoid tariffs through the US-Mexico-Canada Agreement; while Europe has taken the opportunity to attract investment in midstream materials and strengthen localised production.

Key data: in 2023, China’s lithium battery exports increased by 87% year-on-year, but the proportion of exports to the United States has dropped from 35% to 18%, and the industry chain ‘de-risking’ trend is obvious.

* The next 10 years : three major trends in the lithium battery industry*

Accelerated technology substitution: Solid batteries, sodium-ion batteries and other new technologies may break the existing pattern, reduce the dependence on lithium resources, and thus weaken the impact of tariff barriers.

Regionalised supply chains taking shape: The world will form a ‘China-US-Europe triple-pole’ model, and automakers will need to set up localised production capacity in each region to avoid policy risks.

The rise of the circular economy: U.S. local battery recycling companies (such as Redwood Materials) will benefit from the policy tilt, used battery ‘urban mine’ or become a new battlefield.

* Conclusion: Beyond the Game, Global Collaboration is Needed*

The essence of the tariff dispute is the struggle of countries for the right to speak in the new energy era. However, climate change knows no boundaries, and lithium batteries are not only a commodity, but also a key tool for achieving carbon neutrality. Policymakers need to be wary of ‘zero-sum thinking’ – if trade barriers are allowed to override climate goals, humanity may pay a greater price. For ordinary people, the outcome of this game will directly determine whether we can embrace a cleaner future at an affordable cost.

End

*********************

LYTH Battery is not only a supplier of lithium battery cells, but also a professional manufacturer of lithium battery modules and packs. We don’t use gradient utilisation battery types . No matter for individual cells, battery modules or packs, LYTH only use full new A grade cell types which has original testing report .

For more information or to place an order, visit our website or contact our sales team today!

LYTH Completes Delivery of 100 Bespoke 1P12S NMC Battery Modules

LYTH Completes Delivery of 100 Bespoke 1P12S NMC Battery Modules Why Precision Matters? Behind LYTH’s Latest 5,000-Cell Shipment to Austria

Why Precision Matters? Behind LYTH’s Latest 5,000-Cell Shipment to Austria 2026 Cell Price Update | Structural Cost Repricing Underway

2026 Cell Price Update | Structural Cost Repricing Underway LYTH Supplies 400PCS 2P6S 169Ah NMC Modules to Australian Electric Vehicle Integrator

LYTH Supplies 400PCS 2P6S 169Ah NMC Modules to Australian Electric Vehicle Integrator